Yes. You may employ multiple giving approaches each tax year. Please note that the QCD may lower your taxable income, which can impact the amount of deductions available to you in a given tax year.

Can you make a QCD for more than your RMD?

A QCD can be used to meet your required minimum distribution. Your $100,000 contribution limit can include amounts in excess of the RMD payment, however the total annual amount cannot exceed $100,000 per person.

Is there a QCD limit?

The maximum annual amount that can qualify for a QCD is $100,000. This applies to the sum of QCDs made to one or more charities in a calendar year. (If, however, you file taxes jointly, your spouse can also make a QCD from his or her own IRA within the same tax year for up to $100,000.)

Can a QCD be transferred to an IRA?

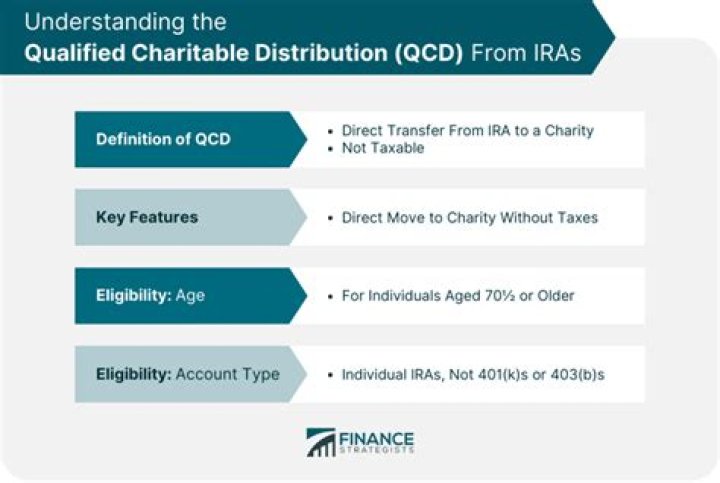

Beware: For some IRA owners, the new law may throw a wrench into their QCD strategy. If you like to give to charity while also trimming your tax bill, the qualified charitable distribution strategy may be your go-to move: IRA owners who are 70½ or older can transfer up to $100,000 per year to charities they support.

How to do a qualified charitable distribution ( QCD )?

How To Do A Qualified Charitable Distribution (QCD) To complete a qualified charitable distribution (QCD) from an IRA to a charity, the IRA owner must: Already be age 70 ½ on the date of distribution. Submit a distribution form to the IRA custodian, requesting that the check be made payable directly to the charity.

How are QCDs split between taxable and non-taxable IRA funds?

If you have basis in a nondeductible traditional IRA, any QCDs you make are considered to come out of taxable IRA funds first. Normally, distributions are split proportionately between taxable funds and nontaxable basis.

Can a qualified charitable distribution be made from an IRA?

To complete a qualified charitable distribution (QCD) from an IRA to a charity, the IRA owner must: While the process of completing a QCD to a charity is fairly straightforward, the key administrative requirement is that the distribution check must be made payable directly to the charitable entity.